Your Equity Superpower: A Simple Formula to Offset a Higher Rate

The number one conversation I have with homeowners in Marion County right now isn't about paint colors or school districts. It’s about a number: 2.75%.

If you bought your home or refinanced between 2020 and 2021, you likely have a mortgage rate that feels like a winning lottery ticket. And because of that rate, you might feel stuck. You have outgrown your current space. Maybe your commute down I-75 has become unbearable, or your family has expanded, and you are tripping over toys in the living room.

You want to move. You likely need to move. And yet, the math of trading a 3% interest rate for one hovering in the mid-6% range feels like financial malpractice.

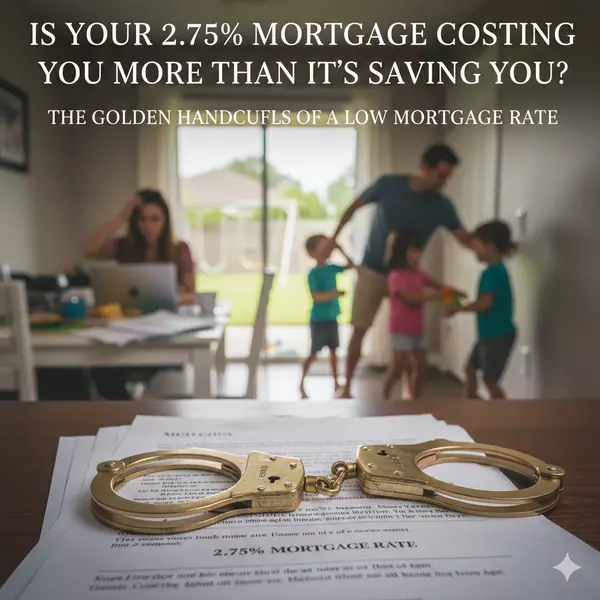

This is the "Golden Handcuffs" effect. It creates a paralysis where you put your life on hold to protect a percentage point.

Here is the reality many move-up buyers overlook. You have a financial tool available right now that you didn't have when you bought your first home. It changes the math entirely. It is the "Affordability Paradox." While borrowing money is more expensive today than it was three years ago, your purchasing power has shifted because of one massive factor: Equity.

Understanding how to use this equity is the difference between staying cramped in a home that no longer fits and comfortably transitioning into the home your family actually needs.

The Reality of the Ocala Market Transition

To understand why your position is stronger than you think, we need to look at what has happened in Ocala over the last five years.

In 2019, the average existing home price in our area was around $149,200. Fast forward to today, and median sales prices have stabilized in the high $200s to low $300s, with specific neighborhoods like Heath Brook and Devonshire commanding significantly more.

If you have owned your home for even three or four years, you aren't just a homeowner. You are an investor who has realized massive gains. That appreciation is real money. It is a savings account you have been contributing to every month, supercharged by the market’s growth.

The mistake most people make is looking at a new mortgage calculator based on the full purchase price of a new home. They assume if they buy a $450,000 house, they are borrowing $400,000.

That is rarely the case for a move-up buyer. Your equity is the variable that offsets the interest rate.

Defining Equity: The Hidden Wealth

Equity is simply the difference between what your home is worth today and what you owe to the bank.

Current Market Value – Remaining Mortgage Balance = Gross Equity.

For example, if your home in Marion Oaks or Silver Springs Shores is worth $300,000 today, and you owe $150,000 on your mortgage, you have $150,000 in gross equity.

This is wealth you have already created. It is sitting in your walls and your land. When you sell, that money becomes liquid. It becomes the superpower that allows you to batter down the monthly payment on your next home, rendering the higher interest rate far less painful than the headlines suggest.

Calculating Your "Usable" Equity

Before we get to the final payment math, we need to be precise. Gross equity is not the number you walk away with. We need to calculate your Net Proceeds. This is the actual check you receive at the closing table.

In Florida, and specifically here in Marion County, selling a home comes with transaction costs. You should estimate that roughly 5% to 10% of your sale price will go toward these costs.

Here is what that includes:

- Commissions: Typically split between the buyer's and seller's agents.

- Documentary Stamp Tax: A state tax on the transfer of real estate ($0.70 per $100 of value).

- Title Insurance: In Marion County, the seller customarily pays for the owner’s policy.

- Prorated Taxes and HOA Dues: You pay for the portion of the year you owned the home.

The Net Proceeds Formula

Let’s run a conservative scenario.

- Sale Price: $350,000

- Mortgage Payoff: $150,000

- Gross Equity: $200,000

- Estimated Costs (~8% for safety): $28,000

$200,000 (Equity) - $28,000 (Costs) = $172,000 (Usable Equity).

You now have $172,000 to apply toward your next move. This is a substantial down payment that a first-time homebuyer simply does not have access to.

The Equity Superpower in Action

Now, let’s look at how this money changes the affordability of your next home.

We will compare two buyers purchasing the same $450,000 home in a neighborhood like Heath Brook.

Buyer A: The First-Time Buyer

They have saved diligently for years to put down 5%.

- Purchase Price: $450,000

- Down Payment (5%): $22,500

- Loan Amount: $427,500

- Principal & Interest (at ~6.4%): ~$2,674/month

Buyer B: You (The Move-Up Buyer)

You are rolling your $172,000 of usable equity into the purchase.

- Purchase Price: $450,000

- Down Payment (Equity): $172,000

- Loan Amount: $278,000

- Principal & Interest (at ~6.4%): ~$1,739/month

The Result: Even though you are buying a significantly more expensive home and paying a higher interest rate than you have now, your massive down payment slashes the monthly obligation.

You are paying nearly $1,000 less per month than someone buying the same house without your equity advantage.

This is how you beat the rate. You borrow less money. By reducing the principal balance so drastically, you minimize the impact of the interest rate on your monthly budget.

The Cost of Waiting vs. The Cost of Moving

The financial math is clear, but we also need to weigh the lifestyle math.

I often ask clients: "What is your plan after you sell?"

If the answer is that you need to be closer to good schools like Forest High or West Port because you are spending ten hours a week in a car line, that time has a value. If you need a home office because your current internet connection in a rural area is threatening your job, that connectivity has a value.

Waiting for rates to drop is a gamble. Historically, when rates drop, buyer demand surges. When demand surges, prices rise.

If you wait two years for rates to drop to 5%, but home prices in Ocala appreciate another 5-10% in that time, you might end up with a lower rate on a more expensive house. Your monthly payment could end up being exactly the same, but you lost two years of living in the home you actually needed.

We call this "Marrying the house and dating the rate."

If you buy now, you secure the asset price. You use your equity to keep the payment manageable. And if rates drop in the future? You refinance. You cannot renegotiate the purchase price of a home three years from now, but you can always renegotiate the debt.

Thoughtful Consideration for Your Next Step

Moving is not just a financial transaction. It is a life transition. And frankly, sometimes the right answer is not to move.

I am not going to lie to you to get your listing. If the numbers don't make sense for your specific goals, I will tell you to stay put.

But if you have been feeling trapped by your current mortgage rate, you need to look at the full picture. You are likely sitting on a financial tool that can unlock the door to the next chapter of your life.

Your equity is your superpower. It is the bridge between the home you have outgrown and the lifestyle you are trying to build.

Don't let a percentage point dictate your family's future. Let’s look at the real numbers together.

Book a 15-Minute Clarity Call.

Categories

Recent Posts

Broker Associate | License ID: BK3161032

+1(352) 426-2706 | c@christineandpartners.com